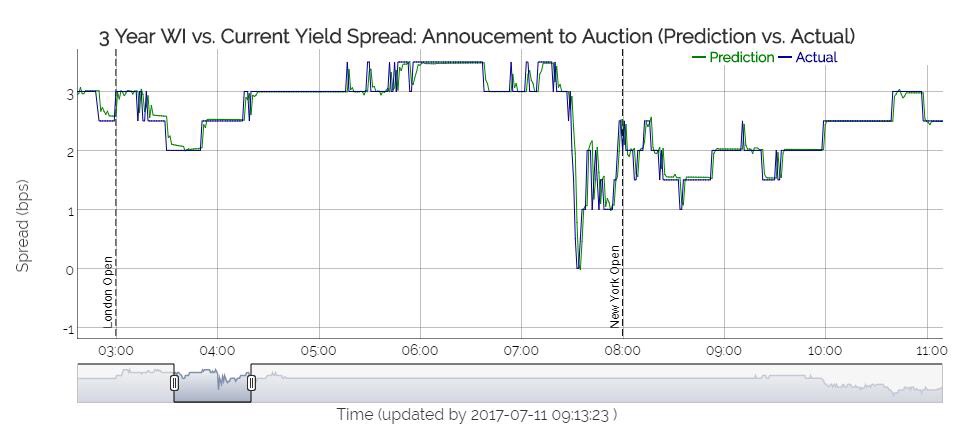

Predict the Auction

An auto-regressive time series model has been applied to the treasury auction process every month to closely monitor what is happening on site. We’ve managed to output a nice prediction on the auction spreads (WI – old until auction date and current – old until settlement date) on a rolling window basis (approximately a two-hour window), which enables traders to closely monitor the market and trade based on our predictions. Our predictions have achieved high accuracy in terms of direction prediction and have a mean square of error of less than 0.1%.